2025 in numbers:

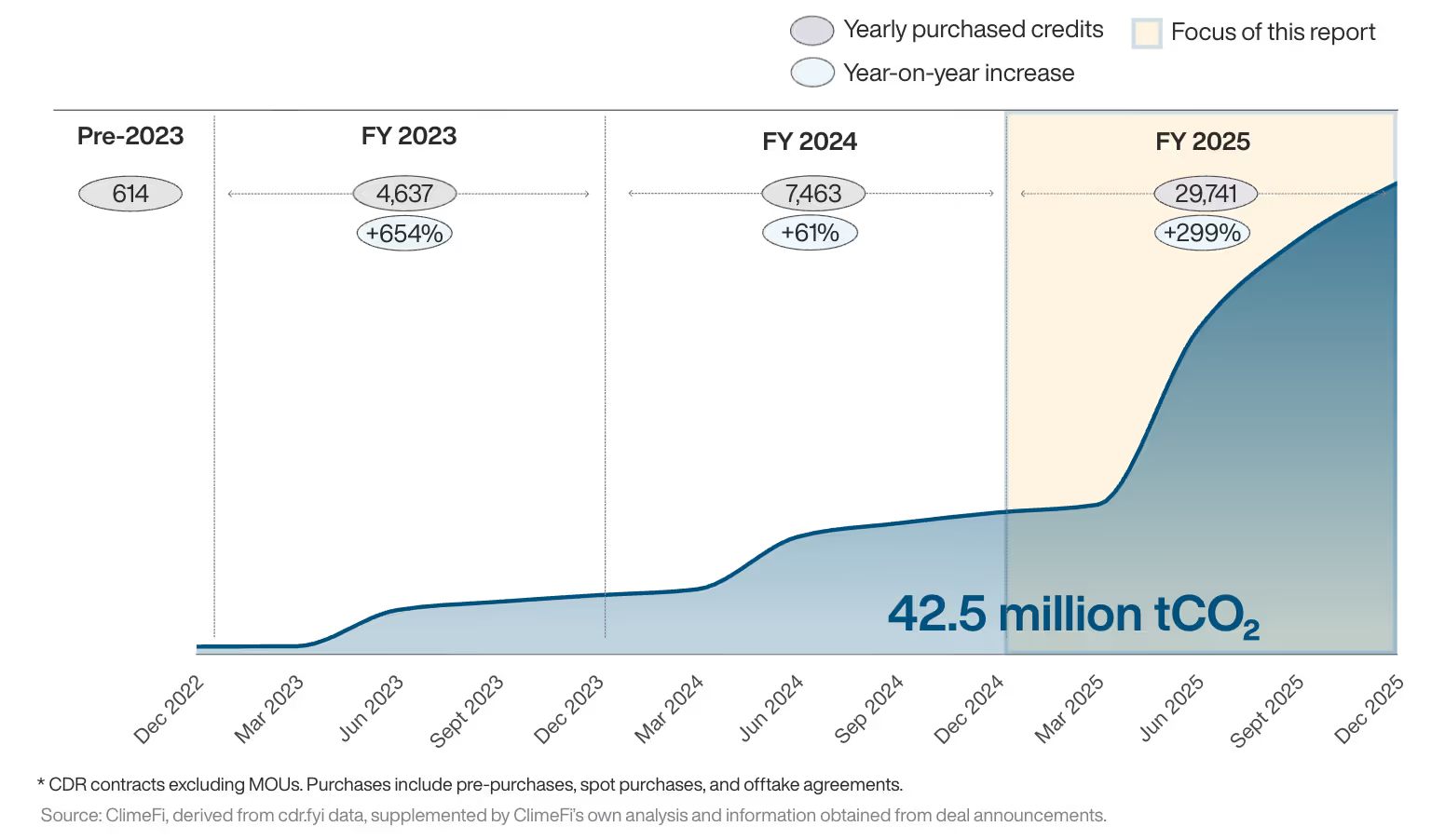

Durable carbon dioxide removal (CDR) underwent a fundamental phase shift last year, with the market recording a massive 299% year-on-year growth in new contract volumes compared with 2024.

Figure 1: Cumulative CDR market commitments (ktCO2)

With 29.6 million tonnes of new contracts signed (cumulative total commitments now stand at 42.5 million tonnes) 2025 will be remembered as the year that the market shifted from small pilot deals to megatonne transactions. Q2 2025 alone recorded over twice the amount of purchase volume than the whole of 2024.

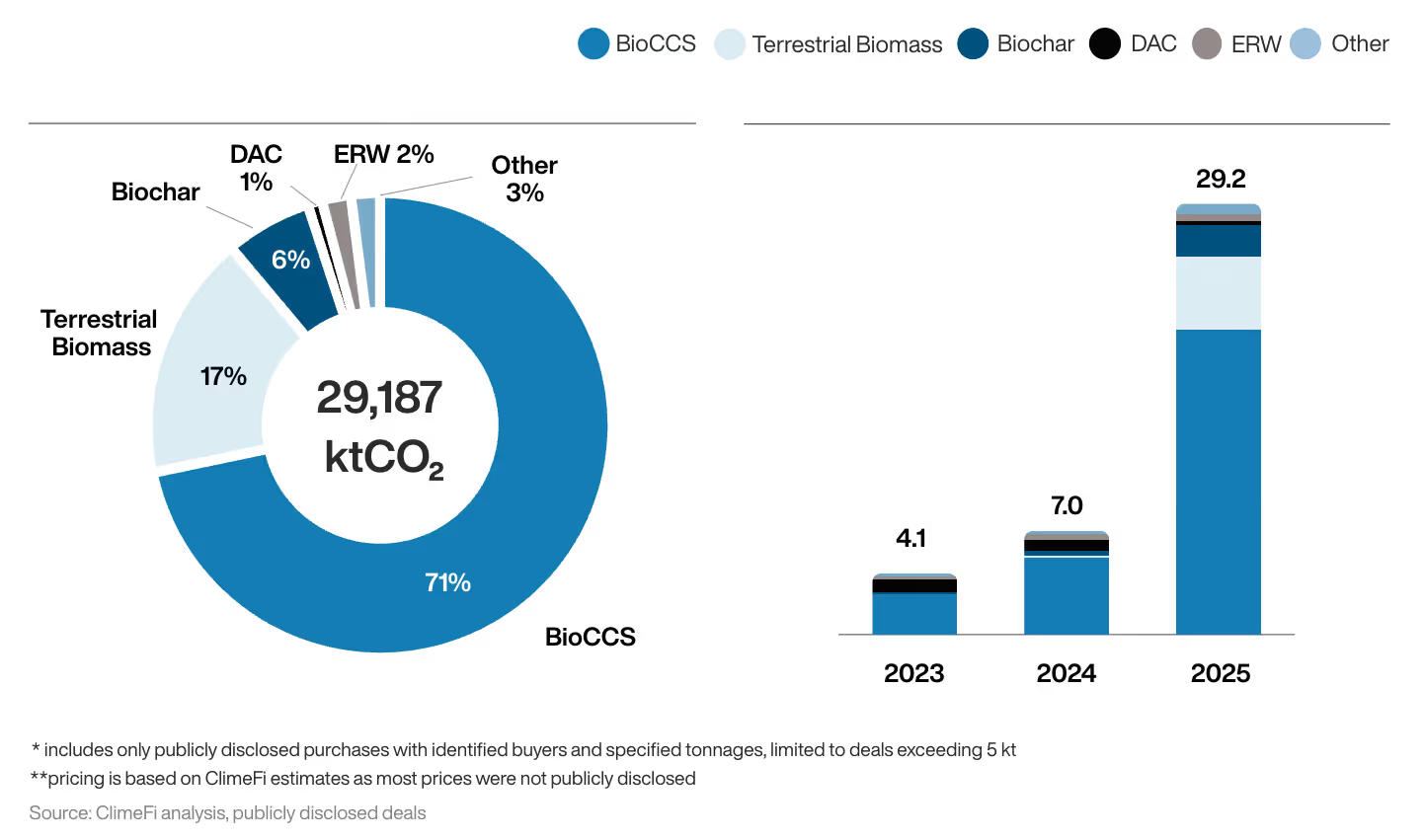

Figure 2: 2025 key purchases (ktCO2) / 2025 key yearly purchases (MtCO2)

While BioCCS remained the leading driver of purchase volumes in 2025 for the third year in a row, Terrestrial Biomass emerged as a breakout star, surging to 17% of total volumes from just 2% the previous year.

In terms of purchase value, BioCCS has skyrocketed in recent years: purchases in 2025 reached $5.3bn, a sixfold increase from the amount spent on BioCCS in 2023. In tandem, the amount committed to DAC has dropped significantly in recent years, from $572m in 2023 to $350m in 2024, and finally to $103m in 2025.

Buyer insights: beyond first movers

While the headlines were dominated by growth, primarily driven by one buyer in particular, the underlying story is one of market maturity and the arrival of a new wave of corporate CDR buyers.

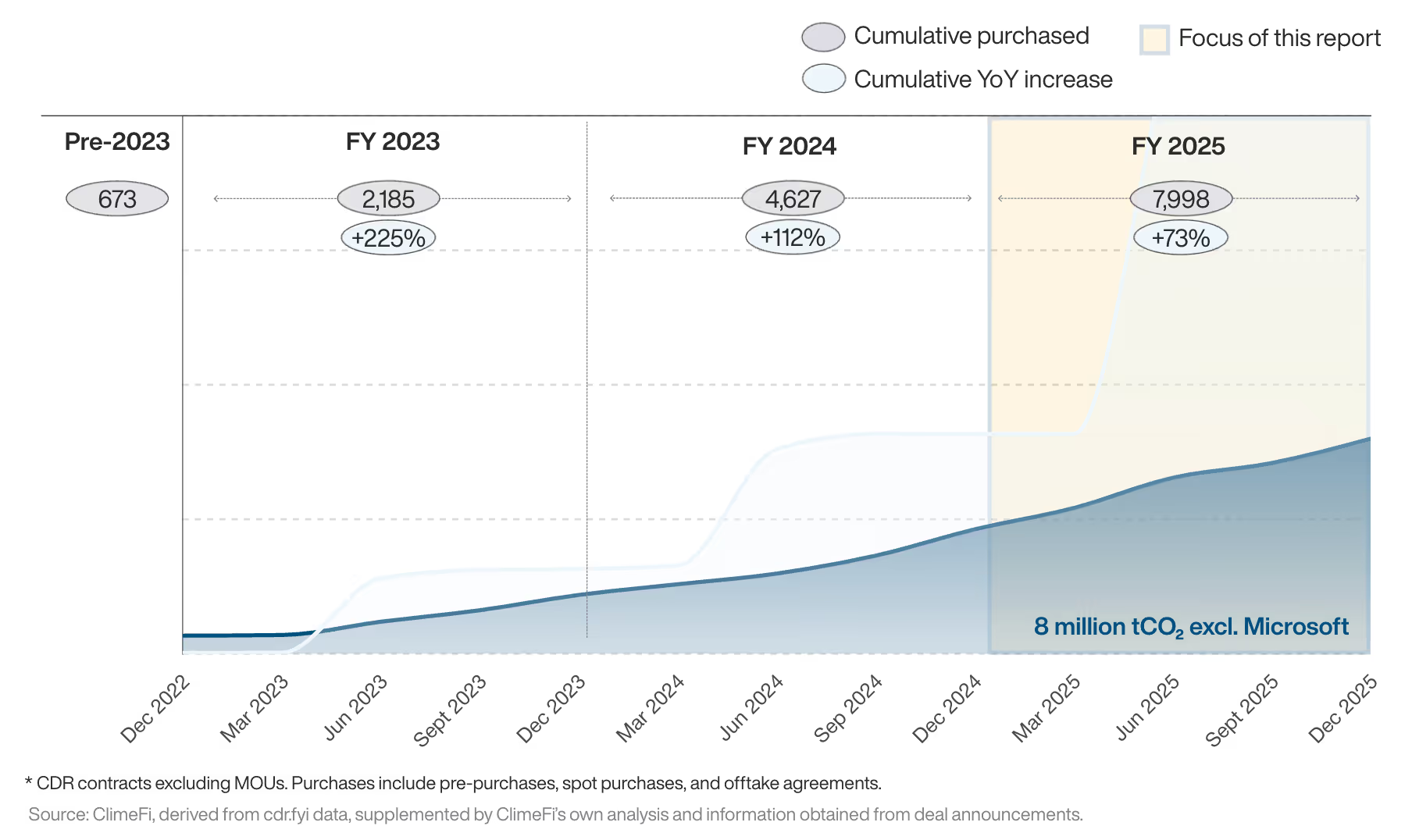

There is no doubt that Microsoft firmly remains the centre of gravity for the CDR market, ending last year with 81% of the total market share. The tech giant’s commitments accounted for 90% of all purchase volumes in 2025, helping a number of suppliers to break ground on building mega-scale facilities.

However, even excluding Microsoft’s outsized influence, the rest of the market grew by 73% YoY, with over 3.3 million tonnes in new contracts. Indeed, Q3 2025 saw 11 unique buyers of CDR, with approximately 20 new buyers entering the market for the first time throughout the course of the year. This shift indicates that the market is moving beyond just first-movers, albeit at significantly lower purchase volumes.

Figure 3: Cumulative CDR market commitments without Microsoft

Project insights

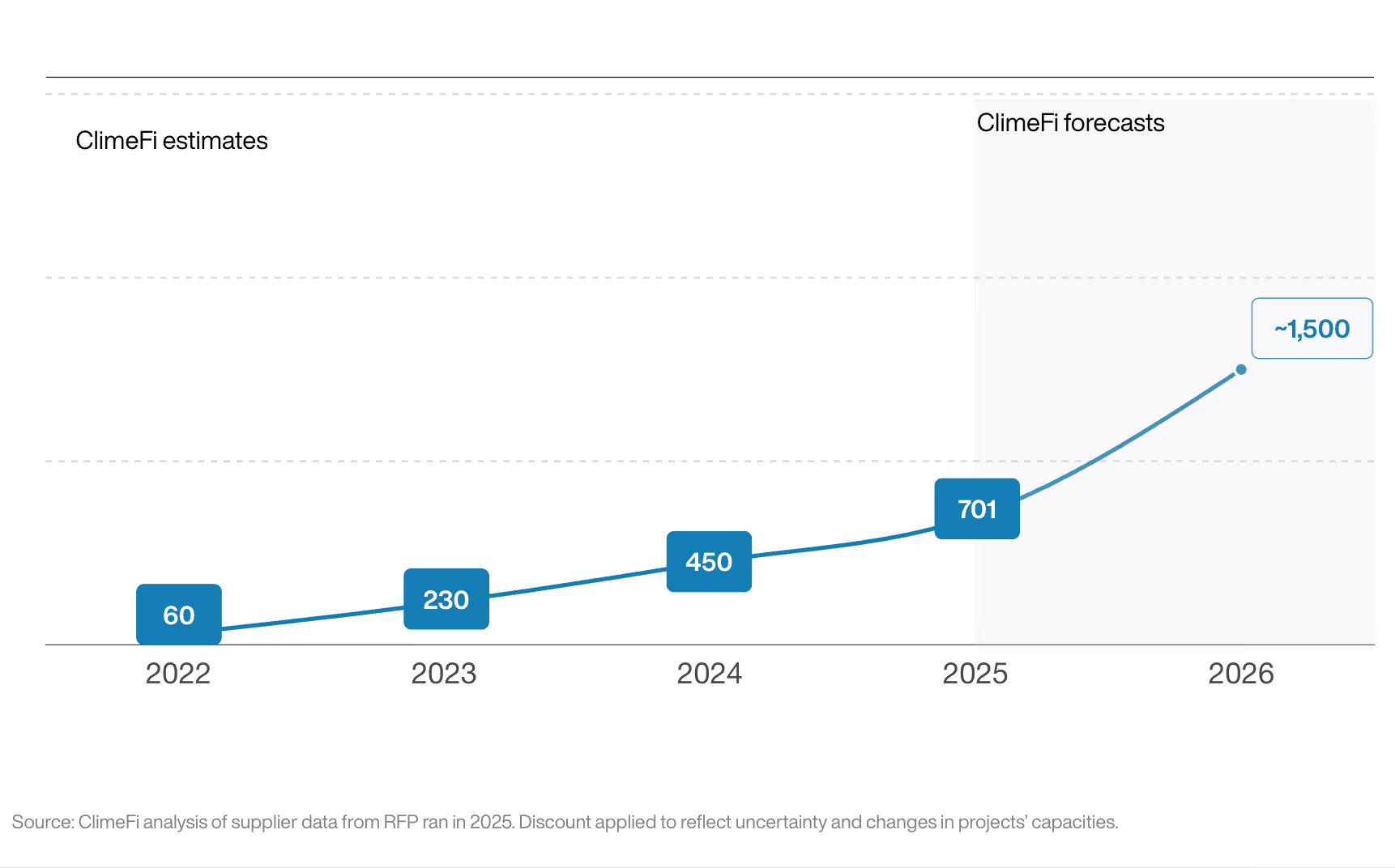

2025 saw a 68% increase in credit issuance, signaling that the supply-side is slowly starting to catch up with the surge in demand in recent years. The top five suppliers accounted for 77% of total issuances, with Gevo – formerly known as Red Trail Energy – emerging as the dominant force, responsible for 52% of all credits issued in 2025. Puro.earth continues to lead in terms of certification, capturing roughly 93% of all issuances on its registry.

Looking ahead, ClimeFi anticipates roughly 1.5 million tonnes of issuances in 2026 – a significant leap from the ~700 ktCO2 seen in 2025.

Figure 4: ClimeFi issuance projections based on key supplier data (ktCO2)

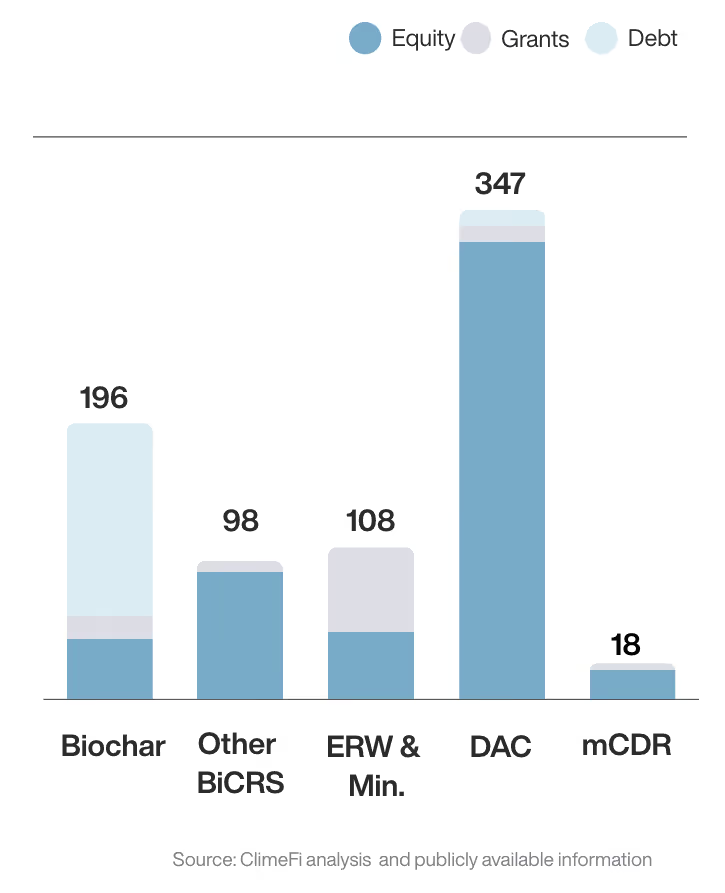

Perhaps the most significant indicator of market health was the shift in how projects are funded. While private funding was down 16% overall, the emergence of new debt financing mechanisms – such as green bonds and innovative credit facilities – marks something of a sea-change for the CDR market, proving that financial institutions are starting to view durable carbon removal as 'bankable' assets.

Figure 5: 2025 private funding by pathway (US$m)

2026 and beyond

1. CDR costs and prices

Over the next five years, ClimeFi's RFP results indicate 37% cost optimisation vs 12% price decrease.

Most biomass-based CDR (BioCCS, Biochar, Biomass Burial) are expected to achieve ~30% cost optimisation in the coming years, reflecting the current maturity of technologies like pyrolysis and CO₂ liquefaction. Less mature approaches at commercial scale, such as DAC and mCDR, offer greater potential for future cost reductions. Pathways with expensive MRV or constrained feedstocks, such as EW and mCDR, may also see additional cost savings over time.

Price trends often lag behind cost optimisation and may even rise initially, as suppliers transition to financially sustainable models.Cost reductions are projected primarily for new projects from 2030, while legacy capacity continues at higher costs. As lower-cost projects gradually replace older ones, more substantial price declines are likely over the longer term.

Download the report to discover the full insights on costs and pricing.

2. Registry outlook

Our RFP results indicate that Puro.earth is expected to remain the leading registry for Biochar, Biomass Burial, and Mineralisation into Concrete; its early acceptance by buyers and mature methodologies for these established pathways position it to continue benefiting from an early-mover advantage

Isometric is emerging as the dominant registry for DAC, mCDR, and bio-oil. As these pathways mature, their technical complexity and evolving standards are likely to favour registries with a higher tolerance for innovation and methodological iteration.

Enhanced Weathering is likely to remain fragmented in the near term. This reflects ongoing uncertainty and limited consensus around MRV best practices, with greater convergence expected only as standards and measurement approaches mature.