As one of the first and only dedicated portfolio managers in the durable carbon removal market, ClimeFi has had a front-row seat to watch the industry develop over the past three years. To date, ClimeFi has facilitated several dozen offtake agreements across the full range of carbon removal pathways, and has been managing several hundreds thousand tonnes of carbon removal assets for our clients.

With our ‘Lessons learned in portfolio management’ series, we aim to turn this hard-won market experience into actionable intelligence.

Over the past three years, we have found that the risk of credit delivery delays – and in some cases, the risk of non-delivery – has been a persistent challenge for durable carbon removal buyers. While industry data suggests that market-wide delays are the norm, we currently observe that 28% of offtake volumes in ClimeFi’s short-term contracted portfolio – both realised deliveries and those with a future delivery date – have experienced or are set to experience delays to credit delivery, while 47% of the suppliers that we work with have experienced, or expect to experience some form of delays.1

In this article, we explore the root causes of these delays, and how a combination of contract negotiation, ongoing project monitoring, and a flexible approach to portfolio reallocation can ultimately help to mitigate delivery risk altogether.

Why do projects experience delays?

For corporate durable carbon removal buyers, project delays aren’t just minor inconveniences; they can significantly impact a company’s ability to meet its environmental targets, complicate budgeting and erode market confidence. But what factors actually cause delays in the durable carbon removal market?

There are several key drivers which contribute to the challenge.

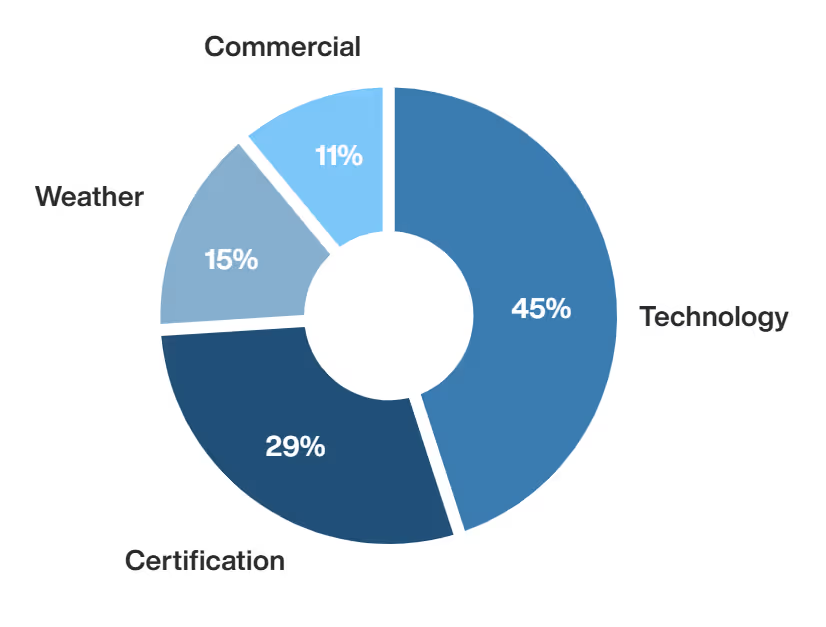

Technology

Among all causes of project delays, technology hurdles have emerged as the leading driver, accounting for 45% of total delays. In a nascent industry, this is perhaps unsurprising: many carbon removal technologies are first-of-a-kind (FOAK), operating under FOAK conditions. Often, these risks compound, leading to unforeseen technical hurdles, engineering complexities, and the need for specialised infrastructure – all of which can lead to delays.

So far, this risk has been identified primarily in relation to Biochar projects: while pyrolysis itself is mature, recent upgrades aimed at boosting biochar yield, enhancing quality, or utilising co-products have caused operational downtime. DAC projects are also at risk, given their novel technology.

Certification

Delays around the certification process come in second, accounting for 29% of total delays. As it stands, several registries are developing FOAK methodologies, while many suppliers are also tackling MRV for the first time. In a nascent market, these factors combined can lead to significant delays.

Enhanced Rock Weathering projects face difficulties on this front, as many methodologies for the pathway are FOAK. These methodologies currently come from various registries, each with a competing view.

Weather

Unpredictable climatic conditions can also significantly disrupt the construction, operation, or maintenance of carbon removal projects. Extreme weather events – events outside the historical averages for a project site – account for 15% of total delays. These can include flooding, high winds, heatwaves, freezing cold, and wildfires, among others.

Commercial

The remaining 11% of delays stem from commercial hurdles. Often, this can be attributed to a project not being able to sell the carbon credits or a co-product from its process. In addition, delays can also result from commercial partners with issues related to feedstock, energy supply, or storage, among other factors.

Mitigating delivery risk

Project delays remain inevitable in any early-stage industry, and mitigating this risk means leveraging every available tool.

Put simply, in order to best mitigate delivery risk, corporate carbon removal buyers need to shift their focus away from ad-hoc purchases and single projects, distribute risk, and enhance the likelihood of achieving climate targets in close alignment with their net-zero timeline.

Key mitigation measures include:

Next up: leveraging contracts

Robust contracting measures, coupled with continuous monitoring of projects until delivery, provide the essential levers to help buyers to navigate the complexities of durable carbon removal project delays.

In the next article in the series, we take an in-depth look at the contracting measures that buyers can take to mitigate these risks from the outset.